I know finance can sound a little tricky, especially when you hear terms like asset-backed securities for the first time. But don’t worry, I’m here to make it simple. Out of all the financial jargon out there, asset-backed securities (ABS) are actually pretty common. In plain words, they’re financial investments backed by loans or debts, like car loans, credit card balances, or leases. These loans bring in regular payments, and that money is passed on to the investors. Sounds a bit complex? No worries. In this blog, we’ll walk you through everything you need to know about asset-backed securities, how they work, and why they matter, step by step.

Check out this table; it has a simplified version of what you need to know.

Check out this table; it has a simplified version of what you need to know.

Understanding Asset-Backed Securities?

So, what do they actually mean? Let me simplify it for you. Asset-backed securities (ABS) are a type of security that’s backed by real-world assets. That means loans or receivables, like car loans, credit card balances, or student loans, are bundled together to form something investors can buy. It simply means it’s a good thing for investors. Now, even if you are a newbie, you might have heard terms like “ABS security” or “asset-backed investment.” These just mean a financial product supported by an asset pool, a group of similar loans. When you invest in an ABS, you’re buying into the cash flow generated by those underlying loans. Each time borrowers make payments, a portion flows directly to you as the investor.How Asset-Backed Securities Work?

Credit: corporatefinanceinstitute.com

Here’s how asset-backed securitization plays out in simple terms:- Lenders create loans (like car or personal loans).

- These loans are bundled into asset pools.

- Through a process called securitization, the pool is converted into ABS securities.

- Investors buy those securities.

- As borrowers make payments, those funds are distributed to the investors.

Why Are Asset-Backed Securities Important?

In the world of ABS finance, these products serve several major purposes:- First, they free up capital for lenders, allowing more funding for new loans.

- They provide fixed-income opportunities for investors.

- Another important thing is that they increase liquidity in the ABS market.

- Lastly, they allow risk to be spread across many loans rather than concentrated in one.

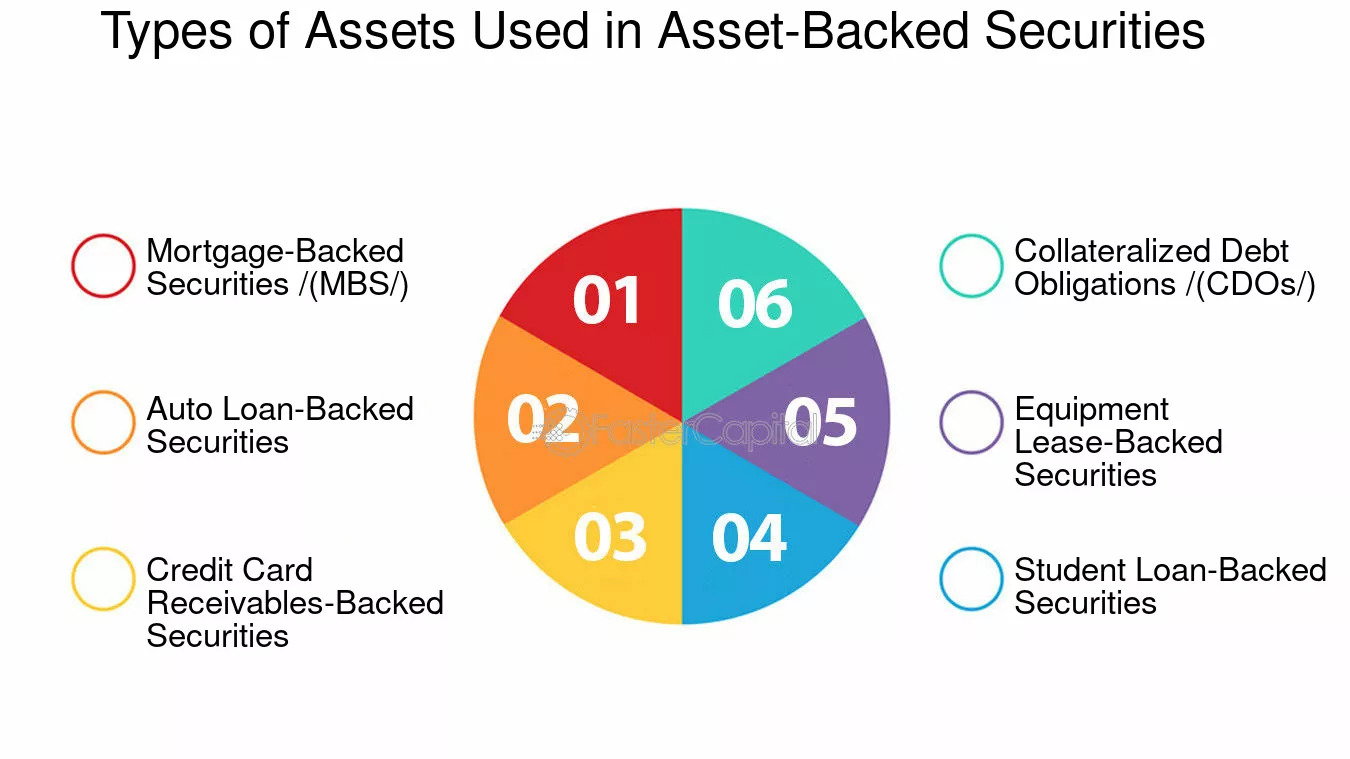

Different Types of Asset-Backed Securities

Credit: fastercapital.com

Well, now let’s talk about the different types of asset-backed securities you might come across:Auto Loan ABS

As the name suggests, these are backed by car loans. They’re common and typically short-term. Such ABS can even involve lease incentives received from dealerships.Credit Card ABS

Next, we have credit card ABS. It is backed by unpaid credit card balances and offers variable interest rates and high liquidity.Student Loan ABS

Built on student loan repayments. Often longer in duration and linked to government or private lenders.Equipment Lease ABS

Based on payments from leased business equipment. A classic case of converting ROU assets into investor income.Personal Loan ABS

And lastly, we have personal loan ABS, which includes installment or unsecured consumer loans. Each type has a unique structure depending on borrower behavior, credit enhancement strategies, and loan terms.Benefits of Asset-Backed Securities

Credit: altline.sobanco.com

Now the question is: why do investors like ABS? Here’s the bright side of the story.Regular Cash Flow

Well, ABS offers a steady stream of cash flow from the loan payments in the underlying asset pools.Diversification

Because each ABS includes hundreds or thousands of loans, it helps spread out credit risk.Shorter Duration

A significant benefit is that, compared to corporate bonds or mortgage-backed securities, many ABS have shorter terms, making them more flexible.Potential for Higher Yield

So, do you know that some ABS tranches offer higher yield than standard bonds, especially if they carry a bit more risk? Yes, it’s true.Risks of Asset-Backed Securities

Of course, with reward comes risk. Here’s what to watch for:Credit Risk

If borrowers default, investors might not get the full cash flow expected. So, it’s not a bright side.Prepayment Risk

Some loans may be paid off early, affecting your income stream.Complex Structure

Some ABS structure models are hard to understand, especially when layered into tranches.Market Sensitivity

Changes in interest rates, borrower behavior, or economic trends can impact performance, just like with ABS bonds or mortgages.Ready to Make Smarter Investment Moves?

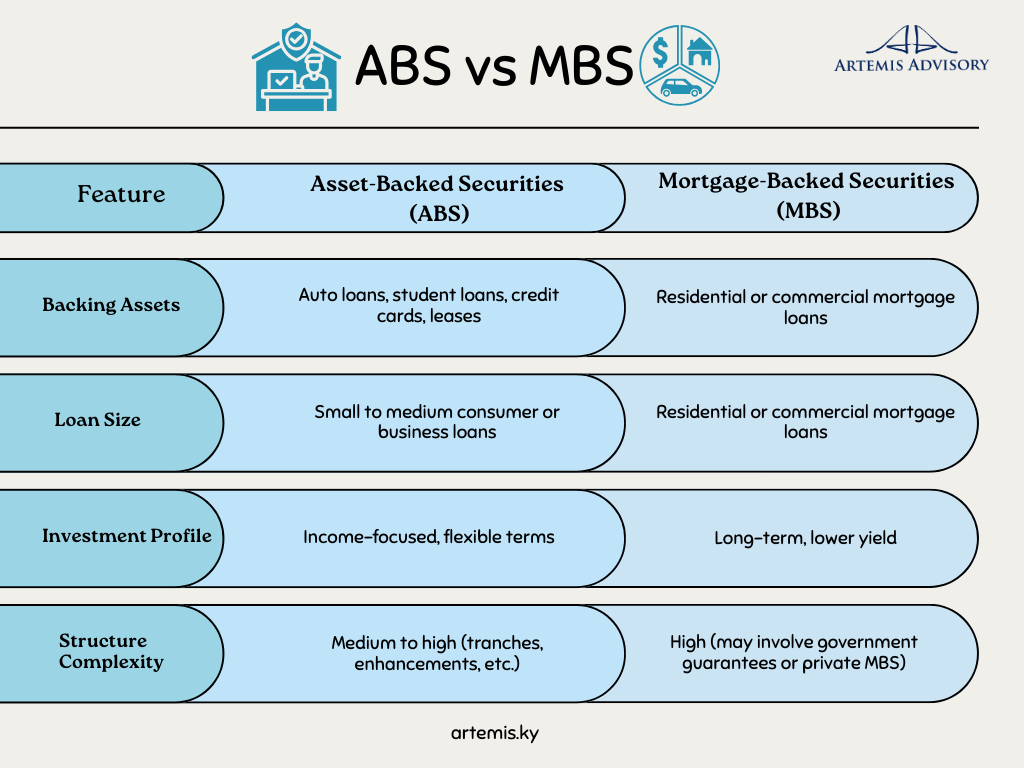

Understanding asset-backed securities is just the beginning. No matter if you’re curious about ABS structure, evaluating fixed income options, or deciding between bonds and ABS funding, getting expert advice can make all the difference. At Artemis Advisory Services, we help you break down complex investments into smart, strategic choices. From understanding the ABS market to diversifying your portfolio with higher-yield opportunities, we’ve got your back. Don’t just invest; invest with clarity. Let Artemis help you find the right opportunities that match your goals. Contact us now.ABS vs MBS: What’s the Difference?

Let’s make this simple. Both ABS and MBS are part of the securitization world, but they differ in what’s backing them.

Check out this table; it has a simplified version of what you need to know.