You know those weeks when life is moving at 100 mph—you’re juggling work, family, maybe even trying to remember if you fed the dog… and tracking your investments? Yeah, not happening. That’s exactly when discretionary fund management steps in, rolls up its sleeves, and says:

“Don’t worry—I’ve got this.” No more late-night stress Googling “best stocks to buy right now.” No more guessing games about whether to hold or sell. Instead, you hand the reins over to a professional portfolio manager who does all the thinking, researching, buying, and selling for you—based on your financial goals, risk comfort, and life plans.

So let’s break it down, in plain English—

👉 What it is

👉 How it actually works

👉 And how to know if it’s the right fit for you

No fluff. No finance-bro jargon. Just real talk.

First Things First: What Does “Discretionary” Even Mean?

Discretion means giving someone the authority to make decisions on your behalf. In this case, it means allowing a fund manager or portfolio manager to buy or sell assets in your investment account—without asking you every single time.

This setup is known as a discretionary mandate—a fancy way of saying, “Hey, you’re the expert. Manage my money.”

What Is Discretionary Fund Management?

Let’s keep it real: not everyone wants to monitor the stock market or obsess over when to buy or sell. That’s where discretionary fund management (or DFM) steps in—it’s like hiring a financial pro to take the investment wheel so you can focus on… well, literally anything else.

Here’s what it actually means

- You hand over full discretion to a trusted financial advisor or investment firm.

- They make the day-to-day decisions—what to buy, when to sell, and how to allocate your money.

- No calls every time a trade happens. They manage your investment portfolio based on your goals and comfort with risk.

- You just sit back and watch your money (hopefully) grow—with updates and reports, of course.

You still get

- A customized strategy based on your financial goals

- Access to expert knowledge and tools

- Freedom from micromanaging your account

- Peace of mind knowing your investments are being looked after

It’s basically like having a personal money manager who eats, sleeps, and breathes the market—so you don’t have to.

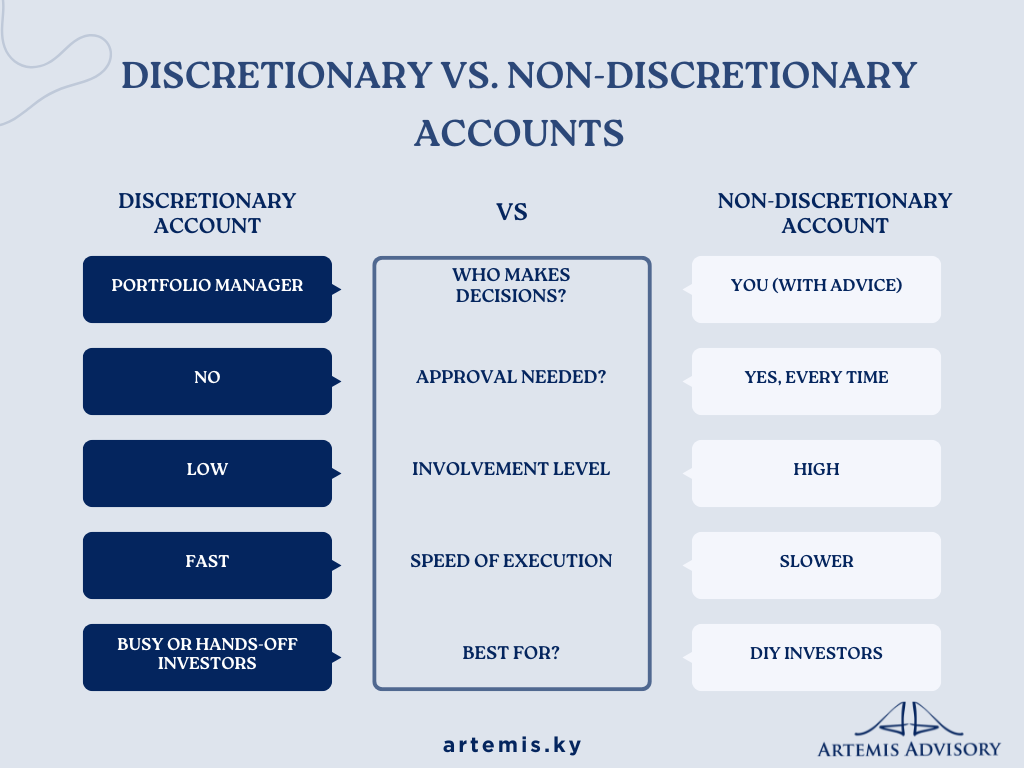

Discretionary vs. Non-Discretionary Accounts: What’s the Difference?

When it comes to investment accounts, the terms discretionary and non-discretionary get thrown around a lot—but what do they actually mean for your money, your choices, and your financial goals?

Let’s break it down in simple terms.

What Is a Discretionary Account?

A discretionary account is one where you give full discretion to your portfolio manager to make buy or sell decisions on your behalf. You don’t need to approve each trade. The manager uses their judgment based on your financial goals, risk tolerance, and the discretionary management mandate you agreed to when opening the account.

Key Features:

- Full discretion to make trades

- No need for client approval each time

- Hands-off investing style

- Ideal for busy investors or those who want professional management

Example: You’ve hired a financial advisor and told them your objective is long-term growth with moderate risk. They’ll handle the day-to-day investment decisions based on that mandate, without asking for your go-ahead each time.

What Is a Non-Discretionary Account?

A non-discretionary account, on the other hand, gives you control. Your financial advisor or portfolio manager may recommend investments—but you must approve each one before anything happens.

Key Features:

- No trades without your say-so

- You stay actively involved

- Ideal for DIY investors or those who want to stay in control

- You can still get advice—but you make the final call

Example: Your advisor calls to suggest buying a new tech stock. You think it over, maybe do some research, and then say yes or no. Nothing moves until you decide.

Trust vs. Control: What Matters Most to You?

Credit: csmltd.com

When choosing between a discretionary and non-discretionary account, it comes down to two things:

- Trust: Do you trust your manager’s discretion to make smart investment choices without your input?

- Control: Or do you want the final say on every move within your investment portfolio?

There’s no right or wrong—only what works best for your personality, investment style, and financial planning approach.

Why High Net Worth Individuals Love Discretionary Management?

If you’ve got a complex financial life, juggling multiple income streams, or aiming to grow serious wealth, discretionary investment management can be a lifesaver.

Here’s why many high net worth individuals choose this route:

- Time-saving: You don’t need to watch the market like a hawk.

Expertise-driven: Managers craft custom investment strategies for you. - Objective decisions: Emotions are out. Logic is in.

- Tailored portfolio: Built to match your financial goals, risk level, and time horizon.

What Does a Discretionary Portfolio Manager Actually Do?

Your managed discretionary account is more than a set-it-and-forget-it deal. Here’s what your portfolio manager handles:

- Asset selection based on performance and market analysis

- Ongoing rebalancing to match your portfolio management mandate

- Monitoring market trends and adjusting your investment portfolio accordingly

- Ensuring you have sufficient to cover future goals or liabilities

- Timing decisions to optimize returns and reduce risks

They take care of the nitty-gritty, so you can focus on the big picture.

How Does the “Discretionary Allotment” Work?

Credit: pccwealth.com

Think of a discretionary allotment like a budget your manager uses to move funds around. They don’t need to call you every time they want to reallocate your investments—because they’ve been given full discretion.

And yes, it’s completely legal and regulated, with clearly documented mandates to ensure your financial institution acts in your best interest.

DIMC Meaning – Just in Case You’ve Seen That Term

You may have come across DIMC in the financial world. It stands for Discretionary Investment Management Company. These are licensed firms that offer managed account services under regulatory frameworks.

They specialize in overseeing your wealth with professional skill—often used by private clients and institutions alike.

What About Net Pay Due and Pay Periods?

You might see terms like net pay due or pay period in discretionary reports. These refer to how dividends, bond coupons, or sale proceeds are calculated and reflected in your account. Your manager ensures that these are tracked and reinvested—or paid out—based on your preferences.

Again, all without you needing to lift a finger.

Is Discretionary Fund Management Right for You?

Credit: finczech.com

This route makes sense if:

- You want a hands-off approach to investing

- You’re not glued to your trading app

- You trust professional fund management

- You’re after long-term wealth building, not short-term hype

- You’re working with a trusted financial advisor or investment firm

But if you like total control and don’t mind micromanaging your investments, then non-discretionary accounts may be more your style.

Need a Reliable Discretionary Management Partner?

If you’re exploring tailored investment decisions through a trusted and experienced team, check out the wealth management services offered by Artemis. They specialize in helping clients reach their financial goals through expert-led portfolio management strategies—built around you.

Closing Remarks

Summing up, choosing discretionary fund management doesn’t mean walking away from your money. It means empowering professionals to act in your best interest—so you can focus on what matters most while your money works smarter behind the scenes.

Because when it comes to growing wealth, sometimes the smartest move… is letting go.

SMART MOVES START WITH TRUST!

Frequently Asked Questions

Here are the most common questions about discretionary fund management:

What is discretionary fund management?

Discretionary fund management is a type of investment service where a portfolio manager makes investment decisions on behalf of the investor. The manager has the discretion to buy and sell assets based on the investor’s objectives and risk tolerance.

How does discretionary fund management work?

The investor grants the fund manager the authority to manage the investments in the portfolio, making decisions without the need for approval on each trade. The manager will aim to meet the investor’s financial goals while managing risks.

What are the benefits of discretionary fund management?

Discretionary fund management provides professional expertise, time-saving, and personalized investment strategies. It allows investors to have their assets managed by experienced professionals, leading to potentially better returns and effective risk management.

What is the difference between discretionary and non-discretionary fund management?

In discretionary fund management, the manager makes investment decisions without seeking approval from the investor. In non-discretionary management, the investor must approve each decision made by the manager.

How do I choose the right discretionary fund manager?

When selecting a discretionary fund manager, consider factors such as their experience, track record, investment philosophy, and communication style. It’s also essential to ensure they align with your financial goals and risk tolerance.

Ready to Make Smart Investment Decisions?

At Artemis Advisory, we specialize in discretionary fund management, offering personalized investment strategies tailored to your needs. Let our expert team help you grow and manage your wealth efficiently. Contact us today to get started!