Need fast cash but still need to use your asset?

Let’s say you own something valuable—a building, a car, or even a piece of machinery. It’s crucial for your daily operations. But now, you need a quick cash injection—maybe to invest in growth, cover expenses, or just improve your cash flow. Selling the asset sounds like a good way to get the money… but then you’d lose access to something you rely on.

That’s where a leaseback (or sale-leaseback) comes in. It’s a clever financial move where you sell the asset to a buyer and then lease it right back from them. You get a lump sum of cash upfront, and you keep using the asset like nothing ever changed—usually under a long-term lease.

It’s a win-win:

- You free up cash that was locked in your asset

- You avoid taking out a loan or giving up equity

- You continue business as usual

From real estate to transportation to manufacturing, leasebacks are helping businesses stay agile and financially strong. Let’s take a closer look at how this works—and why it might be the smart strategy you didn’t know you needed.

What Is a Leaseback?

A leaseback, also called a sale-leaseback, is a financial arrangement where you sell an asset but continue using it by leasing it back from the buyer. Sounds clever, right? That’s because it is!

Here’s how it works in plain English:

- You sell something valuable—like a building, a vehicle, or a piece of equipment.

- Then, you immediately lease it back from the buyer under a formal agreement.

- You continue using the asset as usual, while the buyer (now the new owner) earns rental income through your lease payments.

Basically, you become the lessee, and the buyer becomes the lessor—even though the asset hasn’t gone anywhere.

This setup is especially popular in:

✔️ Real estate deals, where businesses sell commercial property to raise cash

✔️ Contract manufacturing, where companies lease back machinery or production space

✔️ Auto deals, like leasing back a car you just sold to a dealership

It’s a great way to boost cash flow without disrupting day-to-day operations. You get the money you need now—and still get to use what you just sold.

How Does a Sale-Leaseback Work in Real Estate?

In sale leaseback real estate deals:

- A company sells a property it owns—like an office or warehouse.

- The buyer leases the real estate back to the seller for long-term use.

- The seller gets immediate cash flow without relocating.

This is especially popular among businesses that want to unlock the economic benefits of ownership without holding the asset on their books.

What Is an Embedded Lease?

Let’s say you sign a service contract for maintaining your office equipment. If that contract involves controlling a specific asset (like a copier) for a period of time in exchange for payment, that’s an embedded lease.

Under ASC 842, businesses must identify if a contract contains an embedded lease—even if the word “lease” isn’t used. Why? Because it impacts how you report assets and liabilities on your financial statements.

Here’s how to identify an embedded lease:

- Does the contract give you control over a specific asset?

- Do you receive economic benefits from using it?

If yes to both, it’s likely an embedded lease.

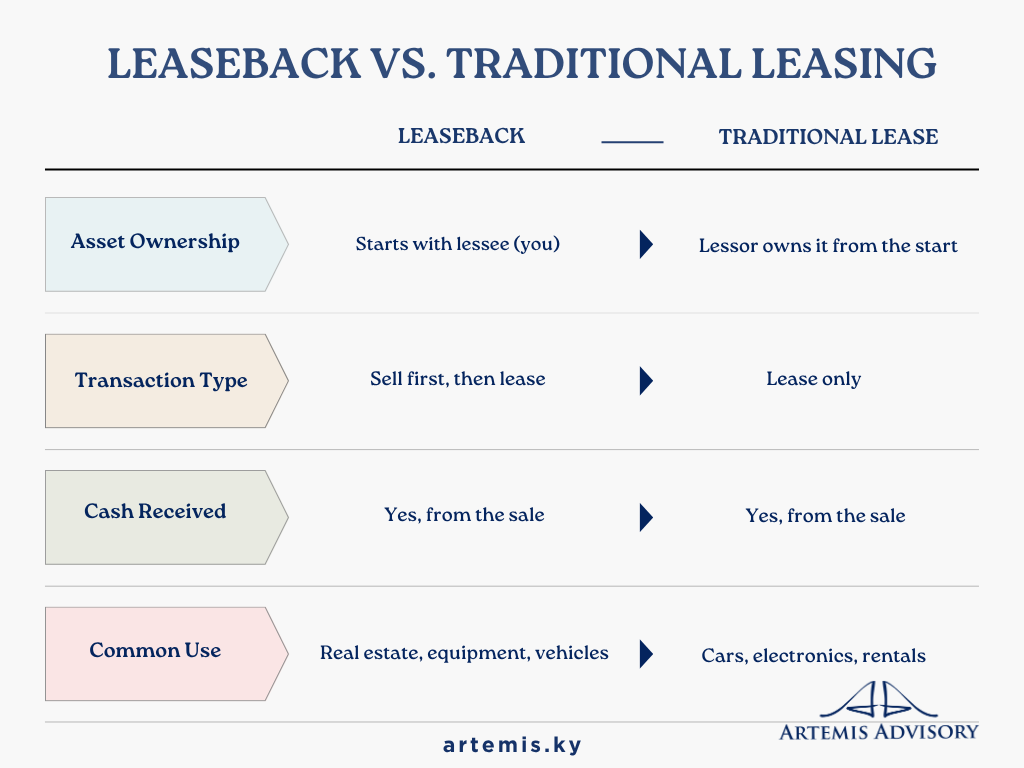

Leaseback vs. Traditional Leasing

At first glance, a leaseback and a traditional lease might seem similar—they both let you use an asset without technically owning it. But look closer, and you’ll see they serve completely different financial goals.

Let’s break it down.

1. Ownership Structure

It’s like cashing out without walking out—you sell it but still get to use it!

Leaseback

- Starts with you owning the asset.

- You sell the asset, then lease it back from the new owner.

- This means you’re now the lessee, and the buyer becomes the lessor.

Traditional Lease

- You never owned the asset.

- You’re simply renting it from the beginning, often without any prior ownership connection.

📝 Key takeaway: A leaseback begins with ownership; a traditional lease doesn’t.

2. Transaction Type

Leasebacks say “money now,” traditional leases say “maybe later.

Leaseback

- It’s a two-part deal: first, a sale, then a lease agreement.

- You’re unlocking equity in the asset, turning ownership into immediate cash.

Traditional Lease

- It’s a straight rental arrangement.

- No asset changes hands, and there’s no sale involved.

📝 Key takeaway: Leasebacks are about raising funds; traditional leases are about temporary use.

3. Cash Flow Benefits

With a leaseback, your asset works double time—use it and get paid!

Leaseback

- You get a lump sum of cash from selling the asset.

- This cash can be used to invest, pay off debt, or boost liquidity.

Traditional Lease

- No cash upfront.

- Instead, you make regular monthly payments to use the asset.

📝 Key takeaway: Leasebacks give you money; traditional leases cost you money from day one.

4. Typical Use Cases

Leasebacks are for long-game thinkers—traditional leases are for quick fixes.

Leaseback

- Often used by businesses to improve cash flow without losing access to important assets.

- Common in:

- Commercial real estate

- Manufacturing equipment

- Corporate fleets or vehicles

Traditional Lease

- Popular for personal and short-term use needs.

- Common in:

- Cars and electronics

- Office rentals

- Retail equipment

📝 Key takeaway: Leasebacks are used for strategic financial planning; traditional leases are usually for convenience.

With a leaseback, you sell the asset to raise funds. In a standard lease, you just rent it—no upfront cash for you.

Why Use a Leaseback?

Credit: eliottdavis.com

Here are some smart reasons businesses choose sale leaseback transactions:

- Free up cash without interrupting operations

- Improve cash flow for reinvestment or debt reduction

- Remove assets from the balance sheet (depending on structure)

- Maintain use of critical product line tools or real estate

It’s like pawning your office… except you get to keep working in it.

⚠️ Risks and Considerations

Of course, leasebacks aren’t perfect. Keep these in mind:

- You lose ownership of the asset

- You must commit to a long term lease, sometimes with fixed rent

- The new owner might impose limits on use or maintenance

Also, under new accounting standards like ASC 842, lease obligations may now appear on your books, even for an embedded lease.

What About Lease Buy Back in Cars?

In the auto world, a lease buy back means you buy the car at the end of a lease. But dealerships may also do the reverse—a buy and lease back deal for people who want to sell their vehicle but still use it.

It’s less common, but it works the same way: sell, then lease.

✍️ The Legal Side: Lease Agreement Structure

Credit: henrybeaver.com

In a leaseback, the lease agreement must clearly lay out:

- Time in exchange for payment

- Description of the specific asset

- Terms of exchange for consideration

This ensures the transaction holds up legally and complies with tax and accounting standards.

So, are you ready to explore smart leasing strategies? Learn more about financial structuring and professional advisory services with Artemis.

Because sometimes the best way to move forward… is to sell and lease back.

The Bottom Line

As we sum up, leaseback can be a smart financial move—whether you’re looking to unlock the value of your real estate, improve cash flow, or keep using high-value assets without ownership headaches.

But like all financial tools, it depends on your situation. Know the risks, read the lease agreement carefully, and consult a pro before signing anything.

LEASEBACKS FREE UP CASH, BUT KNOW THE RISKS BEFORE YOU SIGN!